Wow. The Fed now has an unemployment rate target for asset purchases: 7 percent.

Political Calculations

Unexpectedly Intriguing!

28 June 2013

Thanks to the efforts of the Food Network, many Americans have become familiar with the gourmet food truck craze taking root in many cities across the United States.

What they might not know is that the economics of doing business is really behind the phenomenon. Compared to operating a restaurant at a fixed location, food trucks:

- Can go to where people/customers are, creating more opportunities to generate revenue.

- Tend to have lower ownership and overhead costs.

- Maintain the same food preparation and cleanliness standards as fixed-base restaurants.

There are also a lot of challenges that can go along with owning and operating a food truck, which shouldn't be underestimated.

But all this just sets the stage for a new development that we want to consider: mobile factories.

It's natural to think of this possibility these days thanks to the advances of 3-D printing technology, but we're thinking more old school. What about putting a factory on wheels to support limited production runs for small producers, who haven't yet developed the revenue stream or the creditworthiness to invest in their own permanent production facilities to produce the kind of stuff for which 3-D printing just isn't cost competitive?

Perhaps something like a mobile cannery for local craft brewers?

Gives a whole new meaning to the idea of what a beer truck can be now, doesn't it?

The mobile solution might be optimal for these kinds of producers because it's unlikely that the local canning and bottling operations for large-scale firm would contract with the small producers to can or bottle their product. Meanwhile, the cost of high volume bottling and canning equipment is such that it's unlikely that any contract canning or bottling firms are available nearby for handling small-scale runs.

But if you can put the equipment for bottling or canning beer on a truck, you can make it possible to grow a craft brewers' business - providing the small-scale service they need to be able to grow beyond the hand-bottling phase. They come to you, where you and your production equipment are, and make it possible for your facility to produce more than it could without a major capital investment.

That's something that wouldn't necessarily be limited to canning or bottling - we think that many packaging operations could be done this way, not to mention a wide variety of other manufacturing or production operations that can be done on a small scale (after all, the entire production facility would be based on a truck!) And really, the only small scale production or operation that couldn't be produced on mobile platforms are things that require high levels of precision, where it would be necessary to anchor equipment to a large vibration-isolated fixed mass to provide the necessary stability to support the production.

We think the economics of the mobile factory business would be very similar to that for food trucks - with many of the same advantages and disadvantages as their fixed, larger competition.

Some of those advantages would be more unique to different kinds of production. For example, if the only thing preventing a particular activity from taking place in a certain area is a local ordinance or regulation, and all it takes to make it economically feasible, not to mention perfectly legal, is to do it on the other side of a city, county or state line, a mobile factory might be a whole lot more cost effective than the cross-country transportation operation that might otherwise be required to reach a fixed-base facility where the job can be done.

On the other hand, suppose the operators of the mobile factories were more like pirates, who wheel in for a job that might not be permitted where its being done, who then drive off as quickly as its done?

When most people think of smugglers, we're pretty sure they think that they only smuggle goods, like cigarettes, or other illicit and highly regulated things. Who's to say that production can't someday be smuggled in just the same way? Or that it isn't already?

27 June 2013

Remember our chart from last Friday, 21 June 2013 - the one that we said wouldn't be sending a "sell signal" until sometime in the next week?

Well, here you go, as we update our chart through Wednesday, 26 June 2013. Now what will you do?

If it helps, what this chart is really saying is that the period of relative order in the market that accompanied the rally that really got underway after 15 November 2012 is over. With the 20-day moving average for stock prices having now moved outside the outer limits of our "normal" target range for this period of order, we can say that the data points falling outside this range aren't just outliers for an existing trend, but are rather evidence that the previous trend itself has broken down.

And yet, the question remains. Now what will you do?

If it helps, let's zoom out and look at the larger scale trend for stock prices. The one that has existed since stock prices stabilized onto an overall upward trajectory following the aftermath of the end of QE 2.0 (our first chart focused on just the region of this chart within the purple rectangle):

Well, that didn't help much, did it? Well, how about this. Our favorite indicator of distress in the stock market, the price-dividend growth ratio (the "G-ratio") appears to have peaked this month. Typically, when that happens, stock prices will go on to hit a significant trough within the next three months, falling from the average level of stock prices for the month in which the peak in the G-ratio occurred.

Now what will you do?

26 June 2013

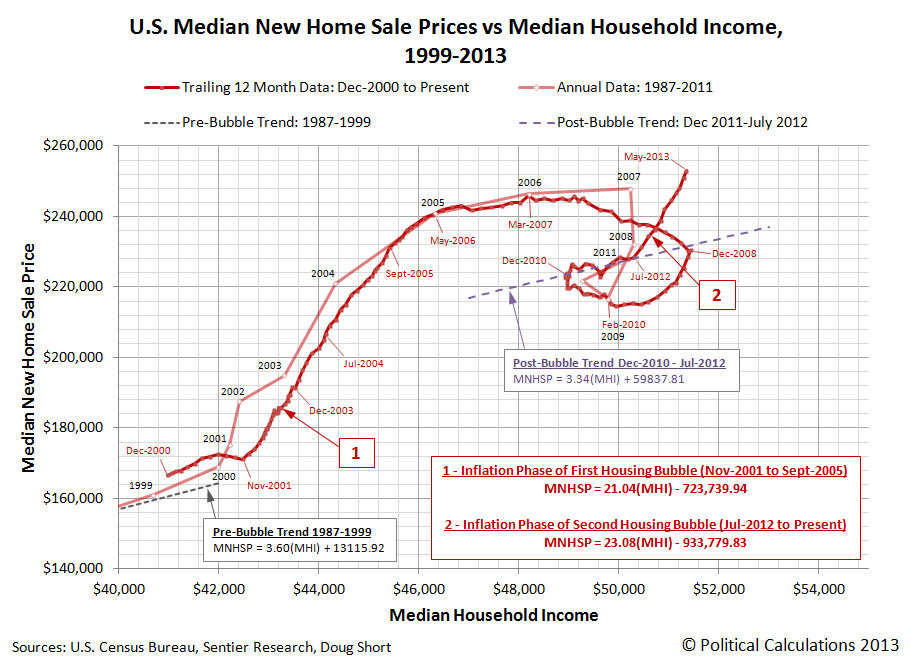

In May 2013, the trailing twelve month average of median new home sale prices in the U.S. continued to inflate, reaching an initial value of $253,033. This marks the fourth consecutive month in which a new record has been set for this particular statistic, which has risen by $2,058 from the previous month's figure.

Meanwhile, the trailing twelve month average of median household income for May 2013 has come in at $51,351, rising by $50 from the figure recorded in April 2013. This value is still short of the record of $51,444 set for this statistic in December 2008, just before the large scale losses of high paying jobs in the U.S. automotive industry took place. [Prior to December 2008, job losses for the recession starting in December 2007 were concentrated among positions that were typically held by young adults and teenagers, where increases in the federal minimum wage in 2007 and 2008 were primarily responsible for the seemingly permanent elimination of hundreds of thousands of these low-income earning positions.]

Our chart below shows the trend for the non-inflation adjusted twelve-month trailing averages of both median new home sale prices and median household income for each month since December 2000:

With the latest update to its Excel spreadsheet detailing median new home sale prices, the U.S. Census has revised its figures for a number of previous months upward. With that updated data, we find that since the second U.S. housing bubble began to inflate in July 2012, the median sale price of new homes has increased on average by about $23 for every $1 increase in median household income. This represents a faster average pace of growth than was recorded during the inflation phase of the first U.S. housing bubble.

The Spark for Inflating the New Housing Bubble

As with the first U.S. housing bubble, which sparked off its inflation phase back in November 2001, the proximate cause of the second U.S. housing bubble is nearly identical: a sudden and very large influx of money flowing into the U.S. housing from the sale of investments in other markets.

In 2001, the dominant source of those funds came from the sale of stocks, whose prices had been originally bid up during the inflation phase of the Dot-Com Bubble from April 1997 to August 2000, which investors first mostly held and then began to sell off in great quantitites in 2001. In 2012, the dominant source of funds flowing into the U.S. housing market came from hedge funds and real estate investment firms, such as the Blackstone Group, which made a strategic decision enter into the residential real estate market using the proceeds it was accumulating from the sales of their previous investments in corporate real estate after good opportunities in that market began to become hard to find.

The influx of these funds into residential real estate markets led to the depletion of the available inventory of homes to historically-low levels in many of these markets, which in turn, led to sharp increases in U.S. new home sale prices compared to more sustainable growth rates, both in 2001 and in 2012, even though investors in both 2001 and in 2012 were primarily focused on acquiring existing homes, and distressed properties in particular in 2012.

That's because new homes are, virtually by definition, at the margin for all real estate markets. Their prices are therefore especially sensitive to changes in the levels of both supply and demand in the overall market.

And that's another reason why our method of tracking median new home sale prices with respect to median household income is so effective at detecting the inflation or deflation of potential bubbles in housing markets in their earliest phases. If we see median new home sale prices racing far ahead of median household income, it's a pretty clear indication that something has upset the established equilibrium within the U.S. housing market.

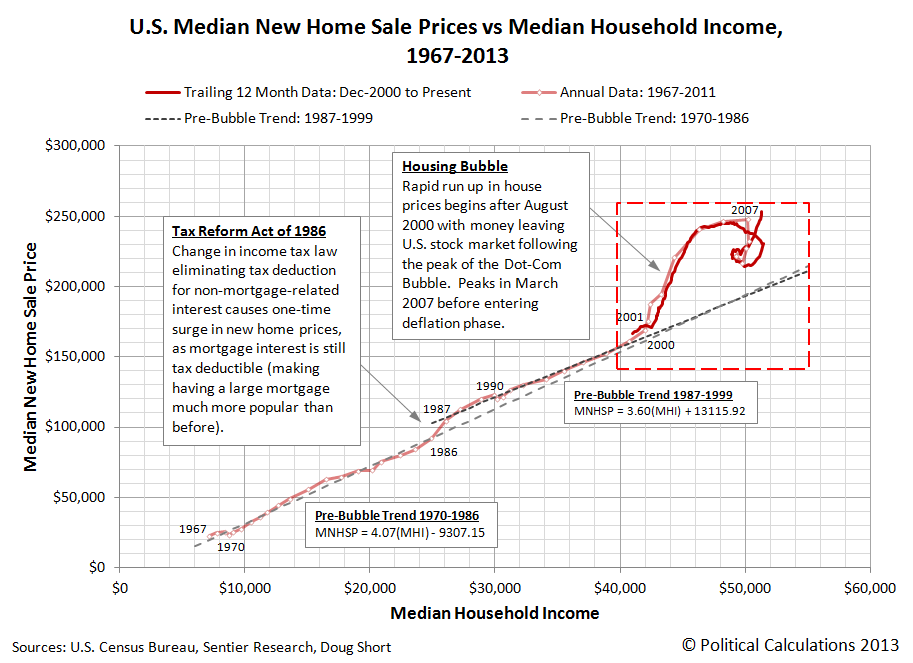

Speaking of which, we'll close with an updated version of our chart showing the long-term view of what established equilibriums for median new home sale prices really look like in the United States:

Since 1967, median new home sale prices in the U.S. have typically increased by anywhere from $3.34 to $4.07 for every $1 increase in median household income in the absence of any periods of bubble inflation or deflation in U.S. housing markets.

References

Sentier Research. Household Income Trends: May 2013. [PDF Document]. Accessed 26 May 2013. [Readers should note that we have converted all older inflation-adjusted values presented in this source to be in terms of their original, nominal values (a.k.a. "current U.S. dollars") for use in our charts, which means that we have a true apples-to-apples basis for pairing this data with the median new home sale price data reported by the U.S. Census Bureau.]

U.S. Census Bureau. Median and Average Sales Prices of New Homes Sold in the United States. [Excel Spreadsheet]. Accessed 28 May 2013.

Previously on Political Calculations

- The U.S. Housing Bubble Is Back - we apply our groundbreaking analytical methods to determine that a new housing bubble has begun to inflate in the U.S. economy.

- Fuel, Oxidizer and a Spark - Part 1 - we revisit the origins of the first U.S. housing bubble and identify the factors that ignited it.

- Fuel, Oxidizer and a Spark - Part 2 - we explain why housing prices rose so much more in just four states than they did elsewhere.

- Fuel, Oxidizer and a Spark - Part 3 - we examine the factors that kept the first U.S. housing bubble going, even after the Fed acted to stop throwing so much fuel on the fire.

- Confirming the Second U.S. Housing Bubble - using revised data, we confirm that there is no apparent new-year slowdown in the inflation phase of the new U.S. housing bubble.

- As the Housing Bubble Inflates: Month 9 - we use hard data to refute the housing bubble deniers!

- As the Housing Bubble Inflates: Month 10 - we note the fourth consecutive record for median new home sale prices and discuss the spark that set off the second U.S. housing bubble.

Labels: real estate

25 June 2013

Which takes a bigger bite out of the economy, government spending cuts or tax hikes?

The chart shows the relative size of the bite that each takes out of GDP as a percentage of each dollar in cut spending or in increased taxes:

What we see is that for every $1 in government spending cuts, the nation's GDP only shrinks by about 60 cents (at least while its unemployment rate is above 7.5%). Meanwhile, every $1 increase in taxes will reduce the nation's GDP by three times that amount below what it might otherwise be.

That's a big reason why over 90% of the fiscal drag on the U.S. economy that the International Monetary Fund is so concerned about is due to President Obama's fiscal cliff tax hikes, and why less than 10% has anything to do with government spending cuts. Not to mention why the IMF is so anxious for the Fed to sustain the pace of its current quantitative easing efforts.

Why do government spending cuts have so much less than a dollar-for-dollar impact? Perhaps the easiest explanation is that about 30-40% of all government spending is wasted in non-value added, non-productive activities that make no positive contribution to the nation's gross domestic product.

Meanwhile, when the government hikes its taxes, it's really acting to penalize the most productive people in the nation to support its wasteful spending activities. The multiplier is so large because tax hikes are so disruptive in their immediate negative effect upon the economy.

By contrast, it takes time for the GDP multipliers for tax cuts to build to the same level of magnitude. That's because it takes time for money to be redirected into more productive activities from where it was before the tax cuts went into effect. Even so, when first implemented, the multiplier for tax cuts is about the same in magnitude as the multiplier for government spending, with the difference being that with tax cuts, there's a positive feedback effect involved that makes its multiplier continue grow to its peak magnitude in about three years time before dropping back slowly, but never fully dissipating.

What's more, these particular GDP multipliers are especially significant because they keep turning up everywhere. For example, if you want to explain why Spain's GDP crashed by the exact amount it did in 2012, look no further than its spending cuts and especially its tax hikes of that year. Or if you want to explain the Greek economic crash of 2010, you can simply look at what its government did in that year to trim its spending and especially what it did to hike its taxes, then apply these multipliers to see how they affected Greece's GDP.

What's more, these particular GDP multipliers are especially significant because they keep turning up everywhere. For example, if you want to explain why Spain's GDP crashed by the exact amount it did in 2012, look no further than its spending cuts and especially its tax hikes of that year. Or if you want to explain the Greek economic crash of 2010, you can simply look at what its government did in that year to trim its spending and especially what it did to hike its taxes, then apply these multipliers to see how they affected Greece's GDP.

They also appear to hold for how the U.S. economy performed in the first quarter of 2013, where fortunately, the Fed's quantitative easing programs more than offset the negative aspects of President Obama's tax hikes along with some pretty trivial government spending cuts after they went into effect. Despite the Fed's action, the U.S. provides the third direct example of these exact multipliers almost perfectly accounting for the negative drag of poorly considered fiscal policies on a nation's economy.

The evidence, by the way, says the exact same multipliers appear to work in explaining how the United Kingdom's economy has behaved over the past several decades.

Given the differences in history, institutions, laws, and the overall structures of their economies, there's really no reason to expect that these seemingly universal GDP multipliers should be so effective in describing the impact of changes in government spending and especially of their tax policies in affecting so many different national economies. That they would seem to have such predictive power is something that perhaps ought to be studied further.

References

Owyang, Michael T., Ramey, Valerie A. and Zubairy, Sarah. Are Government Spending Multipliers Greater During Periods of Slack? Evidence from 20th Century Historical Data. [PDF Document]. Federal Reserve Bank of St. Louis. Economic Research Division. Working Paper 2013-004A. January 2013.

Romer, Christina D. and Romer, David H. [PDF document]. . The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks. [PDF Document]. March 2007.

Cloyne, James. What Are the Effects of Tax Changes in the United Kingdom? New Evidence from a Narrative Evaluation. [PDF Document]. CESIFO Working Paper No. 3433. April 2011.

Labels: economics

24 June 2013

Fed Chairman Ben Bernanke screwed up royally at his press conference on 19 June 2013, as he announced that the Fed's Open Market Committee had moved up its timetable for when it would beginning drawing down its QE 4.0 program.

Fed Chairman Ben Bernanke screwed up royally at his press conference on 19 June 2013, as he announced that the Fed's Open Market Committee had moved up its timetable for when it would beginning drawing down its QE 4.0 program.

QE 4.0, which consists of the Fed's purchases of a net total of $45 billion worth of U.S. Treasuries each month, was originally announced back on 12 December 2012 and was intended to offset the negative effects of the fiscal drag of impending tax hikes upon the U.S. economy in 2013. (Combined with the Fed's QE 3.0 program for buying up Mortgage-Backed Securities, which started back in September 2012, the Fed has been pouring $85 billion per month into the U.S. economy to avoid having it fall into a full blown recession.)

As best as we can tell, it is working as intended.

So why shouldn't the Fed begin tapering its net acquisition of U.S. Treasuries sooner? And why would making an announcement that the Fed was planning to do so be such a huge mistake.

In a single word: timing.

In a single word: timing.

It's difficult to think of how the Fed Chairman could have handled the situation any worse, except perhaps to have put the responsibility for announcing the change in policy into President Obama's floundering hands.

But the key to understanding the huge mistake the Fed has made is not to look at the timing of when the announcement was made, as some influential people are likely to claim, but by considering how it changed the forward-looking focus of U.S. markets.

Investors in those markets are always looking ahead in time - the only real question is how far into the future are the market's most influential investors looking. And when we say "most influential investors", think of the primary owners and majority shareholders of businesses, as well as the people who make decisions at major investment banks and financial firms.

The reason why they do that is because what they expect to happen at certain points in time in the future directly drives their investment decisions. Those decisions, in turn, have tremendous influence over the prices of everything today.

That's because today's prices are really the approximate net present value of the sustainable portion of the profits that might be realized at discrete points of time in the foreseeable future (see here for a more refined definition). What that means is that if you can determine what the expectations are for given points of time in the future, you can work out exactly how far forward into the future the markets have focused in setting today's prices.

With that knowledge, you can then work out how today's prices will change based on changes in those future expectations. While that may sound challenging, in reality, it's complex, but not difficult to do.

For a stock market, the sustainable portion of profits that might be realized at discrete points of time are called "dividends". We can determine what the expectations are for a given point of time in the future by using dividend futures (via IndexArb or the CBOE) to calculate the change that is anticipated in their year-over-year growth rate. We make historic price, dividend and earnings data for the S&P 500 available for free so you can obtain that data as well.

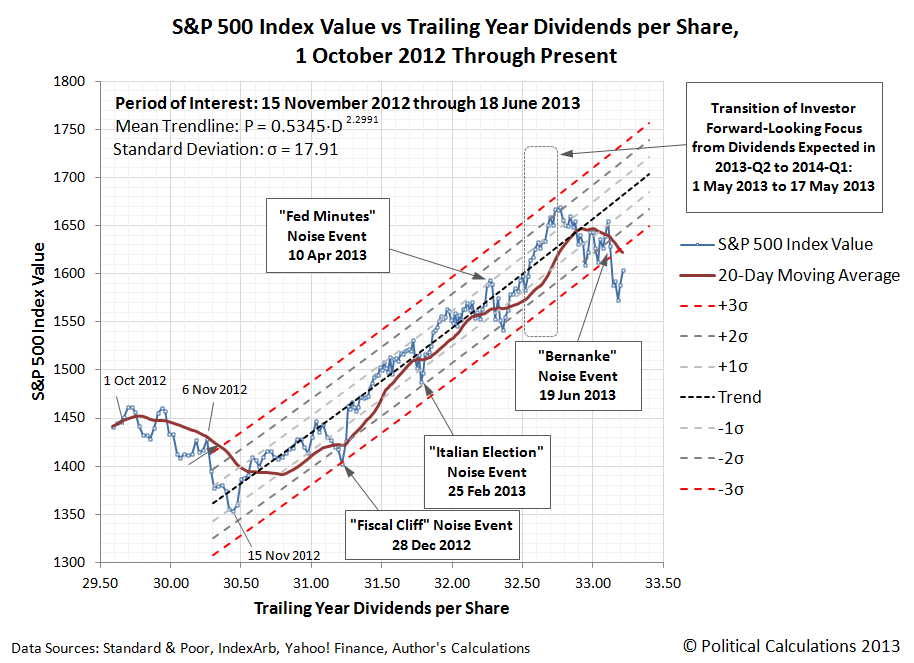

Since late-April/early-May 2013, the U.S. stock market, as represented by the S&P 500, has been focused on the future as given by the expectations associated with the first quarter of 2014. Until about 2:42 PM on Wednesday, 19 June 2013.

At that time, Federal Reserve Chairman Ben Bernanke metaphorically grabbed the noses of the market's most influential investors and forced them to shift their focus away from the first quarter of 2014 to instead focus on an earlier point of time in the future, to either the third or fourth quarter of 2013, which would now coincide with the timing of when the Fed will begin to taper off its QE 4.0 net acquisitions of U.S. Treasuries. Our chart below shows why the Fed's choice of timing in resetting the focus of the market's most influential investors to these particular periods of time is so poor, at least with respect to stock prices:

We estimate that in transitioning from a forward-looking focus upon the first quarter of 2014 to instead focus upon the fourth quarter of 2013, which would be the worst case scenario, stock prices for the S&P 500 would fall on the order of 45-50%, after which stock prices would stabilize at the level prescribed by the expectations for dividends in 2013-Q4. Until perhaps investors could shift their focus to a more promising quarter in the more distant future or an improvement in the outlook for that quarter.

By contrast, shifting their focus even earlier to the third quarter of 2013 would be more beneficial, as that would only involve around a 15-20% decline in stock prices from their 18 June 2013 closing level of 1651.

This analysis assumes that Bernanke's comments succeed in shifting the forward looking focus of investors to an earlier future, which would mark a shift in the expectations for the fundamentals driving the market. At this writing, it is too early to tell if such a fundamental shift has occurred, which is why we are presently classifying the market's reaction as a noise event. Depending upon how the Fed responds to the markets' reaction, it is still possible at this writing to arrest and reverse the decline in stock prices.

Now, we've gone into such basics in this article because we know that Federal Reserve Chairman Ben Bernanke and his successor are going to read it and might like to finally learn a little bit about how things like stock prices actually work. And then, maybe, do something that would shift the focus of investors back to the first quarter of 2014, in a way that ensures the Fed's credibility is not damaged.

Because we're pretty sure the Chairman and his colleagues at the Fed don't want to have to bear the full responsibility for having followed up one colossal error on their watch with another, marked by a second monster stock market rout during their tenure. We just don't think that too many people would want to be able to claim that they surpassed the accomplishments of Roy A. Young, Eugene Meyer and Marriner S. Eccles, the Fed chairmen who oversaw the formation of the Great Depression and the Great Recession of 1937-38.

Labels: chaos, dividends, SP 500, stock market

21 June 2013

So much for a boring summer for the stock market - we might actually have to go into the office. In the mean time, let's get straight to the "selling signal" charts we know you want to see after yesterday's stock market carnage.

This chart shows the most recent combination of microtrends that have existed since 15 November 2012 for stock prices with respect to their underlying trailing year dividends per share, which we're treating as if they were all a single trend by exploiting the fractal nature of stock prices. The one thing that should leap straight out at you is that the daily stock price for 20 June 2013 has fallen well below the "normal" range where we would expect stock prices to be if they were behaving, well, normally. And normally, we would take that as a signal to sell.

But as we've shown previously, this may not be as clear a sell signal as we might hope. It might, after all, just be an outlier for the overall trend in stock prices, and stock prices might quickly go back to be within their "normal" range. And if that's the case, we would find ourselves in the situation where we sold far too soon, where if we chose to re-invest, we would have to buy back into the market at a higher price than where we exited it, effectively losing money in not being able to buy the same number of shares we once owned and of course, the transaction costs.

To avoid that potentially costly situation, we'll concern ourselves more with the trajectory of the 20-day moving average for stock prices, which we'll use as our true signal to sell. Here, if we see the 20-day moving average of the S&P 500's daily closing values drop below the normal range where we would expect stock prices to be if the trend were intact, that will be our more conservative signal to sell.

By doing this, we're trading a little bit of additional short term loss for the potential upside that stock prices might turn quickly around and resume following their previous trend. The important thing to remember though is that we might still be saving ourselves quite a bit of loss to the downside if we waited for a sell signal using the macrotrend (the microtrend in our first chart covers the area inside the purple rectangle on the macrotrend chart).

The key thing to remember about this method is that it works under limited circumstances, and applies only when we've had both generally rising stock prices and more importantly, generally rising dividends per share. Its primary purpose is to help minimize losses after an established trend has clearly broken down.

For what it's worth, we don't expect that we'll see the 20-day moving average for the S&P 500 move outside the "normal" range where we should expect it to be until the middle of next week at the earliest. So certain doom isn't imminent, it's just lurking around the corner.

A couple of days ago, we wrote up an analysis of why stock prices are behaving as they are and will, which we'll be sharing here on Monday, 24 June 2013 as events catch up to it. As least there's that to look forward to next week!...

Previously on Political Calculations

Labels: investing, SP 500, stock market

20 June 2013

See if you can tell from the following chart exactly when Federal Reserve Chairman Ben Bernanke spooked the more timid among Wall Street's professional traders by moving the goalposts closer for ending QE 4.0, the Fed's purchases of up to $45 billion per month in U.S. Treasuries, which it began on 12 December 2012:

For the sake of keeping ourselves interested, we'll present the rest of our analysis in Q&A format....

What time did stock prices start crashing on 19 June 2013?

2:44 PM EDT.

How long does it take investors in the stock market to react to news they weren't expecting?

When then did an unexpected news event occur to which investors negatively reacted?

Sometime between 2:40 PM and 2:42 PM EDT.

What was going on during that time that might have drawn the attention of investors?

Fed Chairman Ben Bernanke's press conference.

What might Bernanke have said within that small window of time to cause such a reaction?

Via the New York Times' live blog of the event:

2:42 P.M. An Unemployment Target Rate

Why did that comment spark such a reaction?

Returning to the New York Times' live blog of the event:

2:45 P.M. Bernanke Explains Unemployment Target

For what might be the first time, Ben S. Bernanke has made policy news at a news conference.

Mr. Bernanke announced an unemployment-rate target at which it might start to taper its asset purchases: 7 percent. Judging by the Fed's own projections, that would mean the taper would be coming toward the end of this year.

The purpose of the announcement is to reduce confusion, it seems. "It was thought it might be best for me to explain that," Mr. Bernanke said at the news conference.

- Annie Lowrey

Was this an accident?

Of course not. Bernanke's comments indicate that the Fed's Open Market Committee wanted it known that the Fed was moving the goalposts for triggering the tapering of QE 4.0. That is something that is projected to happen before the end of this year, which means that the Fed will start tapering off its QE 4.0 Treasury purchases much sooner than what investors had previously been told to expect.

Could this be a huge mistake?

Although investors have been focused on 2014-Q1 since early May 2013 in setting recent stock prices, if investors were to reset their focus earlier to 2013-Q4, for example, the S&P 500 would drop in value somewhere on the order of 45 to 50%, which is the big risk that we've been concerned about for some time.

That outcome would be universally perceived by all observers to be an indication that the Fed's decision to push up the timetable for beginning to taper off its QE 4.0 program was a huge mistake.

How likely is that?

It appears that the Fed expects that the unemployment rate will fall to their new 7% goalpost sometime late in 2013. If investors give the Fed a lot of credibility on that projection, then it will happen.

What about QE 3.0?

QE 3.0 began on 13 September 2012, and consists of the Fed's purchases of $40 billion worth of mortgage-backed securities per month. From all indications, it appears this portion of the Fed's current quantitative easing programs will continue, indicating that the Fed cares a great deal about continuing its efforts to boost the U.S. housing industry, and house prices, at this time.

Does the Fed care about Wall Street's professional investors?

The Fed secretly believes that they're a bunch of pansies.

What will the Fed do next?

What they said they would do. Doesn't Chairman Bernanke have your full attention now?

Where did that goalpost moving picture come from?

Labels: chaos, SP 500, stock market

19 June 2013

Today, we're going to demonstrate how the demands of the International Monetary Fund (IMF), the European Commission (EC) and the European Central Bank (ECB) combined together into a troika to wreck the economy of Greece in 2010.

Let's set the stage. Here is the Guardian's timeline of the major events leading up to the bailout in mid-2010 as they were known at that time. It's definitely worth reviewing to get a sense of the crisis that led to such incredibly poor decisions.

Let's focus now on those austerity measures demanded by the Troika as a requirement to bail out the Greek government from its fiscal crisis. In July 2010, Greece's government reported what that would entail in terms of permanent spending cuts and permanent revenue increases.

Specifically, Greek Prime Minister George Papandreou's government committed to cut €6.915 billion [$9.187 billion U.S. dollars] in the government's planned spending for 2010, while also seeming to commit to permanently increasing the nation's tax collections by €9.950 billion [$13.218 billion USD] in that year.

We say "seeming" because a number of measures mentioned in the report were not enacted, while other amounts were reported as full-year values, where in reality, they were applied for just a fraction of the year. After subtracting the values for the non-enacted measures from the total and adjusting for the actual partial-year data, we find that the Greek government actually increased its intended tax collections in 2010 by €5.971 billion [$7.932 billion USD].

We're going to use those numbers in our tool below, along with the GDP value recorded by the World Bank for Greece in 2009, and also our standard GDP multipliers for government spending cuts and tax increases to see just how close we can get to what actually happened with Greece's GDP in 2010 (we'll also zero out the quantitative easing option, since that's not a consideration in this case). All values are presented in terms of U.S. dollars:

What we find is that virtually all of the decline in Greece's GDP is attributable to the spending cuts and tax hikes demanded by the Troika and enacted by the Greek government, as Greece's GDP fell from $321.016 billion USD [€241.638 billion] in 2009 to $292.305 billion USD [€220.025 billion] in 2010, as our tool is off by just 0.2% from that figure. Of these, the government's spending cuts contributed just 19% of the decline in Greece's GDP, while its tax hikes contributed the remaining 81% of the GDP decline from 2009 to 2010.

The collapse of Greece's GDP was such that the nation was unable to meaningfully close its budget gap, which ensured that the nation's fiscal troubles would be a prolonged experience.

What this chart tells us is that the Greek government only collected about as much revenue in 2010 as it would have without any tax hikes given the size of its GDP for the year. What our math earlier in this post demonstrates is that its GDP would have been much higher if not for its tax increases. (Go ahead! Try it in our tool above!)

On a side note, see if you can tell from our chart above when the next time was that the Greek government implemented additional tax hikes....

Barry Eichengreen describes what might have been for Greece:

The critical policy mistakes were those committed at the outset of the crisis. It was already clear in the first half of 2010, when Greece lost access to financial markets, that the public debt was unsustainable. The country’s sovereign debt should have been restructured without delay.

Had Greece quickly written down its debt burden by two-thirds, it would have been able to shed its crushing debt overhang. It could have used a portion of the interest savings to recapitalize the banks. It could have cut taxes, rather than raising them. It could have jump-started investment and gotten its economy moving again, if not in a matter of months, then, with luck, in no more than a year.

In its official post-mortem on the crisis, the International Monetary Fund now agrees that debt restructuring should have been undertaken earlier. But this was not its view at the time. Under the leadership of Dominique Strauss-Kahn, the Fund was in thrall to the French and German governments, which adamantly opposed debt relief.

Without the benefit of any beneficial monetary policy to offset the disastrous effects of the "balanced approach" demanded by the Troika for its fiscal policies, the wrecking of Greece's economy was ensured.

There are many lessons to be learned here. So far, it only appears that the IMF alone among all the leaders of the world's nations has learned any of them. But then, they still don't appear to have learned the most important lesson that taxes should not be hiked during a recession.

Would it be too much to ask for a fresh slate of more competent leadership all around the world?

References

Hellenic Republic Ministry of Finance. The Economic Adjustment Programme for Greece. [PDF Document]. July 2010.

World Bank. Data: GDP (Current US$). [Online Database]. Accessed 11 June 2013.

X-Rates. Exchange Rage Average (US Dollar, Euro) - 2010. [Online Database]. Accessed 11 June 2013.

Owyang, Michael T., Ramey, Valerie A. and Zubairy, Sarah. Are Government Spending Multipliers Greater During Periods of Slack? Evidence from 20th Century Historical Data. [PDF Document]. Federal Reserve Bank of St. Louis. Economic Research Division. Working Paper 2013-004A. January 2013.

Romer, Christina D. and Romer, David H. The Macroeconomic Effects of Tax Changes: Estimates Based on a New Measure of Fiscal Shocks. [PDF Document]. March 2007.

Labels: economics, gdp, gdp forecast, tool

18 June 2013

![]()

This morning, it appears that our e-mail was temporarily hijacked by a spammer, apparently working out of South Korea, between 11:15 AM EDT and 11:30 AM EDT. Our apologies to all those who unexpectedly heard from "us" during the outburst.

You know, it occurs to us that our friends at the NSA likely already know all about it, including who is responsible for the incursion, and quite possibly are directing drones to the offender's vicinity. And if they're not, just what good are they?...

Labels: none really

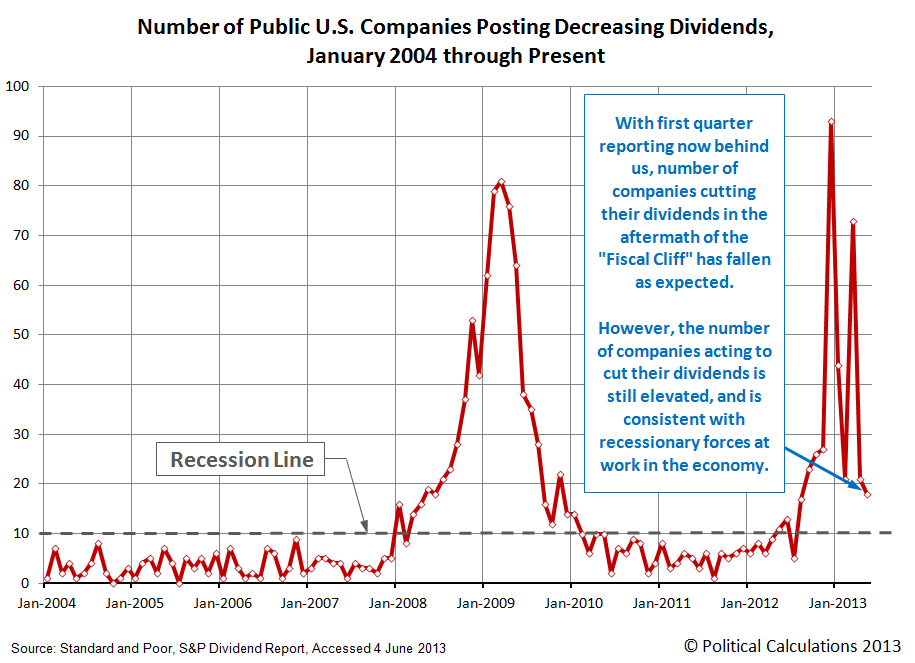

We were busy doing other things earlier this month, but here's the economic situation with respect to dividends in the U.S. stock market through May 2013:

With 18 public U.S. companies acting to cut their dividends in May 2013, the number of companies taking such actions is still consistent with recessionary conditions being present within the U.S. economy.

The level for May 2013 however shows some improvement over previous months, where the number of companies acting to cut their future dividends has been in recessionary territory in all-but-one month since May 2012. We should note that the level of dividend cutting activity in the U.S. was especially elevated from December 2012 through March 2012 as a consequence of the fiscal cliff crisis.

Since that time however, the number of U.S. companies acting to reduce their dividends has gone back to being a pretty solid indicator of general economic conditions in the U.S. We define "recessionary conditions" as being present whenever there are more than 10 public U.S. companies announcing reductions in their dividend payments to shareholders in a month.

References

For those who would really like us to consider a longer timespan in our analysis, if you would, please track down a good source of historic data for the entire U.S. stock market with respect to dividend changes and let us know where it is. Something similar to the following source, which only provides data going back to January 2004:

Standard and Poor. Dividend Action Report. [Excel spreadsheet]. Accessed 4 June 2013.

Of course, if you find such a high quality data source, you're more than welcome to beat us to the punch with your own analysis!...

17 June 2013

As expected, the 20 day moving average of the change in the growth rate of S&P 500 stock prices topped and fell back toward the level where the year over year change in the growth rate of the S&P 500's dividends per share expected for the first quarter of 2014 would have them. Mind the notes in the margin of our chart below and note the differences from the previous version....)

What was different about the past week was a new outbreak of noise in the market, mainly concerned with the future of the Federal Reserve's current quantitative easing programs, which exerted a negative influence that pulled stock prices lower during the week. Here, we can expect a reaction following the Fed's two day meeting this week, with the direction and magnitude of the response dependent upon how convinced serious investors are of the Fed's intentions for sustaining the program.

We'll recommend two posts by Scott Sumner for discussions of why that response matters so much:

To which we'll also point to our own analysis of how the U.S. economy performed in the first quarter of this year:

Like it or not, that's the world investors and the Fed live in now. If it helps, think of today's professional traders who are so distressed over the slightest possibility that the QE punch bowl may be taken away at some distant point in the future as a bunch of pansies that need frequent watering so their confidence can grow....

14 June 2013

You know how it is when you're out shopping. You're looking for the perfect thing, but you're not finding it. In that situation, how long should you keep at it?

You know how it is when you're out shopping. You're looking for the perfect thing, but you're not finding it. In that situation, how long should you keep at it?

Notice that we didn't mention what it is that you might be shopping for.

The truth is that it doesn't matter - we could be talking about anything from apartments for rent to engagement rings made from the finest cubic zirconium, and possibly even your future spouse, and unless you're fortunate enough to recognize perfect when you've somehow accidentally stumbled across it, what you're really shopping for is something that's just good enough to meet your needs.

And to find it, it turns out that you just need to know how much shopping you're willing to commit to do before you've seen enough and can simply buy the next best thing you see.

Emily Oster recently addressed this problem in taking on a question from a young couple seeking a new place to live, but not as yet having much luck in finding suitable accommodations. She writes:

You have, perhaps inadvertently, happened upon an extremely famous area of statistics: optimal stopping theory. The classic example is the secretary problem: you want to hire a secretary, and you have many applicants you interview in order. How do you know when to stop interviewing and hire someone? In your case, how do you know when to stop viewing apartments and just rent one?

Part of what attracts statisticians to this problem is it turns out to have an extremely elegant solution. First, figure out how many apartments you expect to see. Let’s say you think you’ll see 50. The solution says that you should reject the first 50/2.71 apartments (or, about the first 20 of them) and then rent the first one you see after that which is better than any you’ve seen before. (For those of you following the math, the precise number you reject is 50/e, the base of the natural log.)

This is pretty easy to follow and statisticians have proved it will get you the best apartment about 40% of the time, which definitely isn’t 100% but is better than any other strategy!

Well, with that kind of statistical endorsement, how could we possibly pass up the opportunity to build a tool to do the math for you? Just enter the total number of possibilities that you're willing to consider in your search to find what's just good enough for you, and we'll determine the minimum number of possibilities you need to consider to make a decent decision!

For our default example, in a search for where you would be willing to consider up to 50 possible options in your pursuit of the best choice for you, by the time you've considered at least 18 of them, you will have seen enough and can jump at the first opportunity you have that is better than all that you have previously seen.

And, for what it's worth, there's even a 40% chance that you'll be right. Happy shopping!

Labels: geek logik, personal finance, tool

13 June 2013

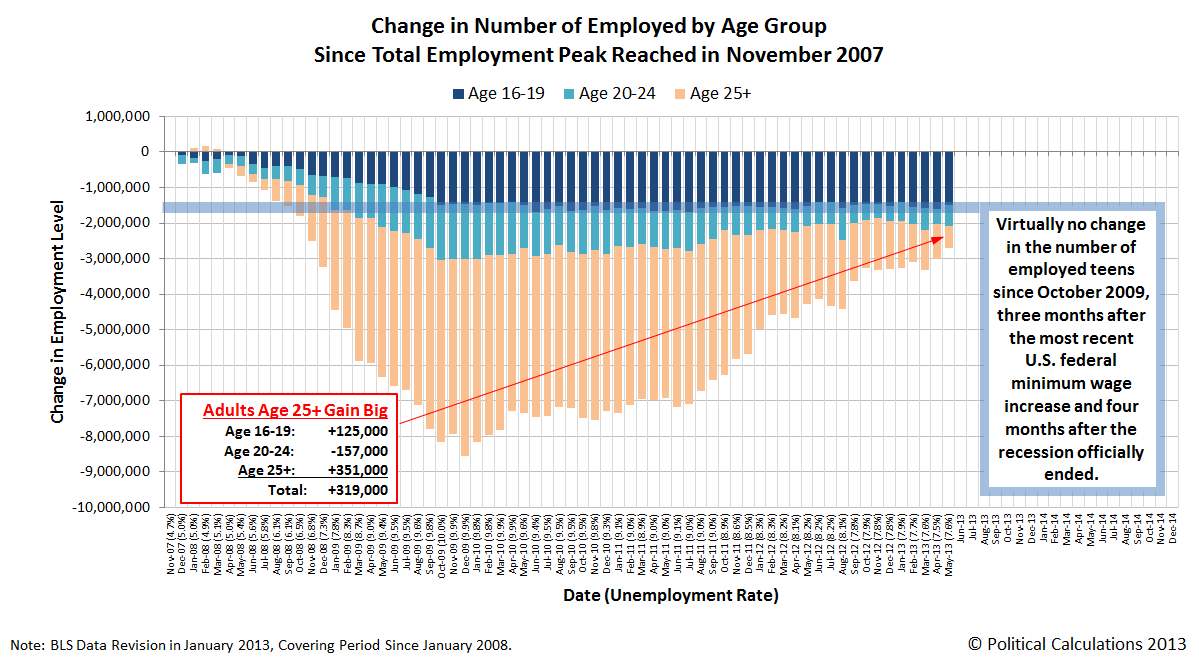

Believe it or not, May 2013 was a good month for jobs in the United States. Unless you're an American teen, where you haven't seen any meaningful improvement in the employment situation since October 2009, or a young adult, where your numbers in the U.S. workforce just fell by 157,000 from their April 2013 level.

But, for Americans Age 25 or older, May 2013 was all good! In fact, for American grownups in the U.S. civilian labor force, it would seem to take just 626,000 more jobs to full recover to the level of employment last seen for this age group in November 2007, just ahead of the Great Recession!

Then again, that includes a lot of U.S. baby boomers, whose numbers are now considerably inflating the ranks of those over Age 65. What about working-age American adults?

Looking just at changes in the Age 25-64 labor force, which we can do by taking the BLS' non-seasonally-adjusted data from the Current Population Survey for the Age 25+ population and subtracting the equivalent data for the Age 65+ population from it, we find that in the six and a half years from November 2007 to May 2013:

- The Age 25-64 population has increased by 4,385,000, from 158,928,000 to 163,313,000.

- The size of the Age 25-64 labor force has increased by just 142,000, from 126,116,000 to 126,258,000.

- The number of employed among those Age 25-64 has fallen by 2,828,000, from 121,653,000 to 118,830,000.

The employment-to-population ratio for American grownups Age 25-64 has therefore fallen from 76.5% to 72.8% in the six and a half years since U.S. total employment peaked in November 2007, even though the population for this segment of working-age Americans has increased by roughly 2.8%.

Likewise, the labor force participation rate for Age 25-64 Americans has fallen from 79.4% to 77.3% during these years, which indicates that about 2% of working-age American adults have become discouraged with the ongoing employment situation in the U.S. and have permanently exited the U.S. work force. Meanwhile, the unemployment rate for working age American grownups who have remained in the civilian labor force has increased from 3.5% to 5.9%.

We find then that the real reason that the Age 25+ population would appear to now be so close to recovering their pre-recession employment number is because about 2.1 million U.S. baby boomers are delaying their retirement as they have retained their jobs into and past Age 65. There's still a very long way to go for a full economic recovery in the U.S.

Labels: jobs

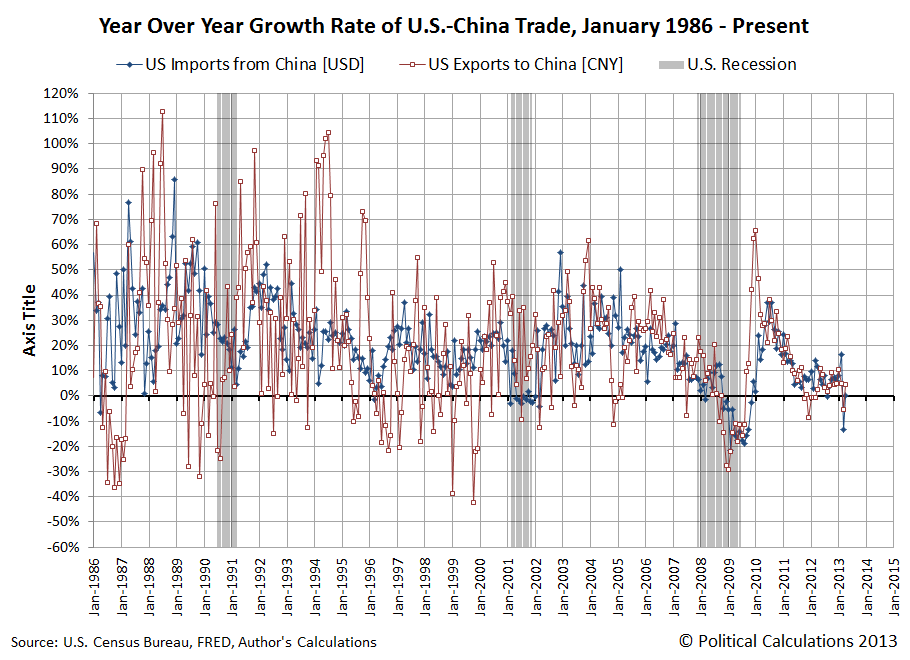

12 June 2013

Following our previous look at trade between the United States and China, we believe we've sorted out much of what happened with China's exports to the U.S. in March 2013.

Here, it appears that much of the fall in the year-over-year growth rate of China's exports that we observed in March 2013 was really tied to the timing of the Chinese New Year/Spring Festival holiday, which effectively ran during the week from 9 February 2013 through 15 February 2013. The late timing of this holiday in 2013 then impacted the volume of cargo from China reaching the U.S.' west coast ports in March because of the 1-1/2 to 3 week long transit time to reach them.

This factor also explains why the year-over-year growth rate for China's exports to the U.S. in February 2013 was so high. The earlier timing of the Chinese New Year/Spring Festival holiday in 2012 placed the holiday-related trough for U.S. imports from China in February 2012.

But what's the real story here with respect to the relative health of the U.S. economy? To find out, we've combined the volume of trade for February and March of 2012 ($59,626.5 billion USD) and also for February and March of 2013 ($60,036.7 billion USD) to calculate the overall year-over-year growth rate for these combined months of 0.7%.

We consider that level to be near-recessionary. Let's next look at the year-over-year trade growth rate data between the U.S. and China for the month of April 2013, which is not impacted by the timing of the Chinese New Year/Spring Festival holiday.

Here, we see that the year-over-year growth rate of the U.S.' exports to China of 4.3% have bounced back to be near their February 2013 level, as there are no historic anomalies in the data (as there were in March 2012). This rate of increase is consistent with a Chinese economy that is growing slowly.

More significantly however, we find that the year-over-year rate of growth of the U.S.' imports from China in April 2013 is 0.3% - less than it was in the combined February-March 2013 period.

We therefore find that U.S. economy is continuing to perform very sluggishly, as it slowly decelerated in April 2013 from an already low level. A more robustly growing economy would be drawing in increasingly higher levels of goods over time.

Labels: trade

11 June 2013

Brian Lucking and Daniel Wilson of the Federal Reserve Bank of San Francisco have made news with their 3 June 2013 Economic Letter, in which they point the finger at a new source of drag on the U.S. economy: the U.S. federal government's fiscal policies, and President Obama's tax hikes in particular (emphasis ours):

While our estimates show that fiscal policy has held back the recovery slightly to date, the effect over the next three years looks much bigger. The CBO projects that the federal deficit as a share of GDP will drop 1.4 percentage points per year over the next three years. This projection would ease slightly to 1.2 percentage points per year if sequestration spending cuts were reversed. By contrast, our calculation of the historical-norm deficit decline through 2015 is 0.4 percentage point per year based on the CBO’s output gap projections. This implies that the excess drag from the rapidly shrinking deficit would reduce real GDP growth annually by between 0.8 and 1.0 percentage point, depending on whether sequestration is reversed. Thus, with or without sequestration, fiscal policy is expected to be a much greater drag on economic growth over the next three years than it has been so far.

Surprisingly, despite all the attention federal spending cuts and sequestration have received, our calculations suggest they are not the main contributors to this projected drag. The excess fiscal drag on the horizon comes almost entirely from rising taxes. Specifically, we calculate that nine-tenths of that projected 1 percentage point excess fiscal drag comes from tax revenue rising faster than normal as a share of the economy. As Panel B shows, at the end of 2012, taxes as a share of GDP were below both their historical norm in relation to the business cycle and their long-run average of about 18%. However, over the next three years, they are projected to rise much faster than our estimate of the usual cyclical pattern would indicate. The CBO points to several factors underlying this “super-cyclical” rise, including higher income tax rates for high-income households, the recent expiration of temporary Social Security payroll tax cuts, and new taxes associated with the Obama Administration’s health-care legislation.

The timing of this particular economic letter from the Fed is cool, because we just did the analysis of the impact of the spending cuts and tax increases upon the U.S. economy in the first quarter of 2013. In that analysis, we found that the Fed's recent adjustments to its quantitative easing programs were working to offset the negative effects of those fiscal policies, which would appear to be the only reason the U.S. economy grew in 2013-Q1.

But more importantly, we also quantified the impact of both the spending cuts and the tax increases upon the nation's GDP. Our tool below focuses just on those components and estimates their relative share of negative impact:

Overall, for the first quarter of 2013, we find that the combination of government spending cuts and tax increases would reduce the United States' GDP by $184.5 billion from the previous quarter, which means the drag of the changes in the U.S.' fiscal policies upon the nation is roughly 1.2% of its GDP, which is close to what the Fed predicts with its model.

Of that fiscal drag on the United States' GDP, 8.5% may be attributed to the effect of government spending cuts at all levels in the U.S. - federal state and local. The remaining 91.5% of that decline is directly attributable to the tax hikes that went into effect in 2013, including the Social Security payroll tax hike, the various Obamacare tax hikes and President Obama's desired tax hikes upon high income earners and investments that were part of the fiscal cliff tax deal at the beginning of the year, all of which applied at the federal government level.

We therefore find that the actual results of the negative effects of the changes in U.S. federal government's fiscal policies are turning out to be pretty much right in line with what the Federal Reserve has predicted using its model.

Previously on Political Calculations

Update 29 June 2013: Reduced the default value for government spending cuts in the tool above from -26.0 billion to -24.2 billion, per the BEA's third estimate of GDP for the first quarter of 2013. We calculate the overall reduction in GDP due to the fiscal drag from tax hikes (92%) and government spending cuts (8%) taking effect in the first quarter of 2013 is 1.1%, which closely agrees with the Fed's prediction.

Labels: economics, gdp, gdp forecast, tool

About Political Calculations

Welcome to the blogosphere's toolchest! Here, unlike other blogs dedicated to analyzing current events, we create easy-to-use, simple tools to do the math related to them so you can get in on the action too! If you would like to learn more about these tools, or if you would like to contribute ideas to develop for this blog, please e-mail us at:

ironman at politicalcalculations

Thanks in advance!

Recent Posts

Indices, Futures, and Bonds

Closing values for previous trading day.

Most Popular Posts

Quick Index

Site Data

This site is primarily powered by:

CSS Validation

RSS Site Feed

JavaScript

The tools on this site are built using JavaScript. If you would like to learn more, one of the best free resources on the web is available at W3Schools.com.

Other Cool Resources

Blog Roll

Market Links

Useful Election Data

Charities We Support

Shopping Guides

Recommended Reading

Recently Shopped

Archives